Intel Vs. AMD: Intel For The Win In 2024 (NASDAQ:INTC)

ugurhan

This month, Intel Corporation (NASDAQ:INTC) and Advanced Micro Devices, Inc. (AMD) lifted the hood on their AI capabilities and plans for 2024. Both companies held their AI events last week: INTC’s AI Everywhere Event and AMD’s Advancing AI Event. We think AMD’s presentation was more attractive than INTC’s in terms of the surprise component, and the stock price movement in response to each event confirms this. AMD stock outperformed INTC over the past 3M by ~10% due to the post-event run-up and chatter around the MI300 series. We continue to prefer INTC over AMD for 2024; we think the former is better positioned to outperform expectations as PC and Server/data center total addressable market (“TAM”) rebound.

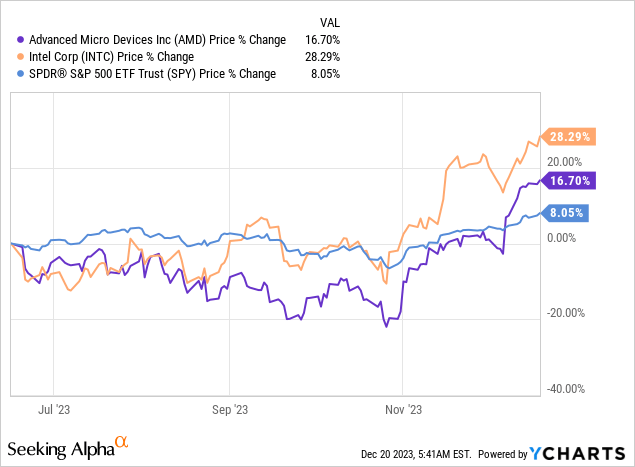

The following outlines AMD’s and INTC’s stock performance against the SPDR® S&P 500 ETF Trust (SPY) over the past 6M.

YCharts

The highlight of AMD’s event was its MI300 series; we think the MI300X will have a handful of customers but don’t expect the product to enjoy the traction of Nvidia’s (NVDA) H100 in sales. We believe AMD’s MI300 series is getting chatter due to Nvidia’s shortage, as demand continues to outweigh supply in the AI accelerator market. We believe NVDA products will remain the go-to-choice in the industry. We also believe INTC has an advantage in its data center sales over AMD, as the latter’s MI300 is the first time the company has made GPU chipsets and bound them in a single system. AMD does have orders for $2B at Taiwan Semiconductor (TSM), but we’re more cautious about the company being able to ship all orders and outpace its guidance.

INTC presented its Gaudi 3 accelerator and new notebook and desktop chips at its event, showcasing its ability to build an AI-focused ecosystem. We saw INTC stock respond less ecstatically than AMD’s stock post-event, as there was little in the way of surprises; management showed investors that the company is on track to uphold Moore’s Law and achieve the process roadmap. We’re also seeing a lot of conversation on the competitiveness of the server market; INTC just launched its Emerald Rapid, the latest generation of Xeon server CPUs competing with AMD’s Geona server CPUs.

In terms of core count, the latter beats the former, but in terms of performance gains, we still think the stage has yet to be set. We think the PC and server/data center total addressable market rebound next year should help improve sales for both INTC and AMD, particularly after the PC slump this year. We estimate the PC TAM to rebound roughly 5-8% Y/Y in 2024. We think AMD will continue to gain share against INTC, but believe the pace of share gain has moderated substantially in comparison to 2-3 years ago. We see INTC share in the market stabilizing now.

Additionally, we do see a higher risk profile for AMD in 2024, as we expect an AI correction sometime next year when supply catches up to demand – NVDA will be the main guide for that correction. We don’t see AMD experiencing material AI demand once the shortage issue is resolved and the market corrects.

Valuation

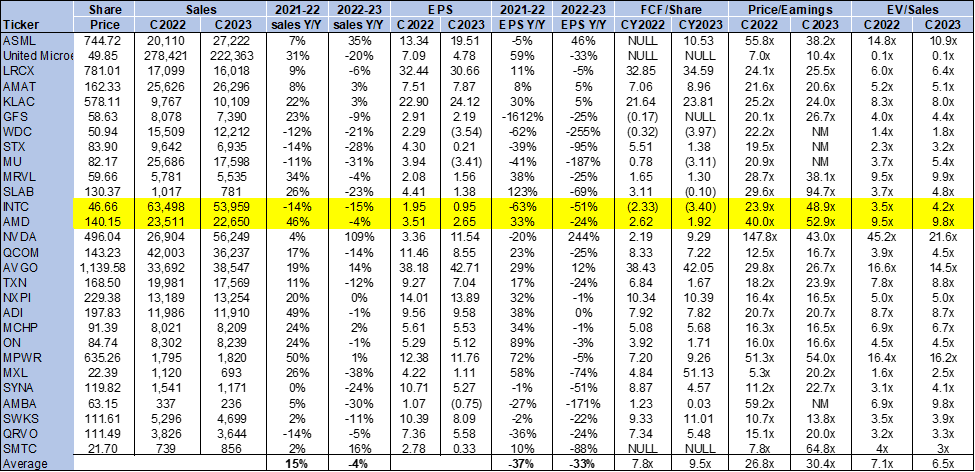

INTC is also more fairly valued relative to AMD, in our opinion. INTC stock is trading at 4.2x EV/C2023 Sales versus AMD at 9.8x, and the peer group average is at 6.5x. On a P/E basis, INTC is trading at 48.9x C2023 EPS $0.95, while AMD is trading at 52.9x C2023 EPS $2.65 compared to the peer group average of 30.4x. We think INTC is better positioned for an upside surprise than AMD, particularly after the latter’s run-up post-AI event last week. Additionally, we don’t think AMD’s higher multiple is justified at current levels; the company presentation was impressive, but we recommend investors be cautious not to get too excited too early about seeing it translated into profit.

The following chart outlines AMD and INTC valuation against the peer group average.

TSP

Word on Wall Street

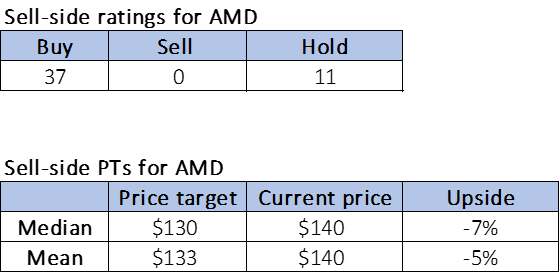

Wall Street prefers AMD over INTC. Of the 48 analysts covering AMD, 37 are buy-rated, and the remaining are hold-rated. The following outlines Wall Street’s sentiment on the stock.

TSP

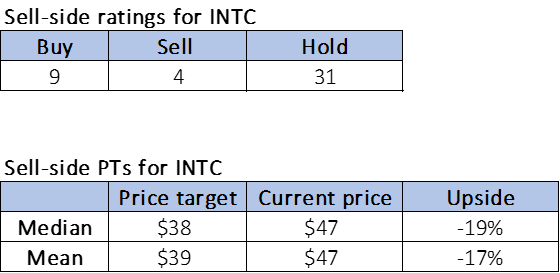

Meanwhile, of 44 analysts covering INTC, nine are buy-rated, 31 are hold-rated, and the remaining are sell-rated. We think Wall Street continues to push the expectation of AMD as the next NVDA, but we don’t see this playing out. We think INTC will be able to more comfortably outpace expectations in 1H24.

The following chart outlines Wall Street sentiment on INTC.

TSP

What to do with the stock

We think Intel Corporation is better positioned to outperform Advanced Micro Devices, Inc. from a fundamental point of view. While investor confidence in AI demand has pushed both stocks higher after their respective events, we see more upside potential for INTC. We do recognize that investor confidence in AMD’s MI300 series may drive the stock higher in the near term, but we believe INTC is a safer investment for the mid-to-long run, as the company is on track to achieve its process roadmap of five chips in four years.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.